When the rubber hits the road for emissions

When the rubber hits the road, will we be on track for smooth sailing?

That’s the question a group of heavy transport companies are currently asking themselves. As part of an SBC collaboration, they’ve set an incredibly ambitious objective to develop a low emissions pathway that will halve emissions from the domestic freight sector by 2030, and be net zero by 2050.

When the rubber hits the road, will we be on track for smooth sailing?

That’s the question a group of heavy transport companies are currently asking themselves. As part of an SBC collaboration, they’ve set an incredibly ambitious objective to develop a low emissions pathway that will halve emissions from the domestic freight sector by 2030, and be net zero by 2050.

The reason for that ambition is two fold. The majority of the collaborators are members of SBC and the Climate Leaders Coalition, so they’ve got their own targets and transition plans in place. And they acknowledge the significant opportunity decarbonising the sector presents in an NZ Inc context. There are solutions available for freight that are being used right now, and so we can make tangible progress while other sectors, such as agriculture, are still at the investigation phase.

What’s great about this group is they represent a broad range of stakeholder perspectives – large freight owners with national coverage – The Warehouse, Countdown and Fonterra; freight movers TOLL, TIL, Swire Shipping and New Zealand Post – who are already implementing a range of low emission options for their customers; and two key points of infrastructure in the network – Ports of Auckland and Lyttelton Port Company.

Our group met for the first time in February to determine what needed to be in scope for the pathway. Since then, our consultants have interviewed each member of the group, and additional enablers to low emissions solutions in the sector including Z Energy, Hiringa Energy, EECA and KiwiRail. At our workshop on Friday they presented their first cut at demonstrating how we could get to the ambitious targets set.

And while some of the solutions are readily available, others have been stopped in their tracks. The ability to add 5% biodiesel to regular diesel blends immediately reduces emissions by 4%. Z Energy invested in plant to manufacture biodiesel from New Zealand tallow, a fatty animal waste-product from meat processing.

However, government policies such as mandates, subsidies and low carbon credits in the United States, UK and Europe mean biodiesel can not only be sold at parity with fossil fuels, it can be highly profitable. This is in stark contrast to New Zealand, where there is no government policy support, and where the most many customers are willing to pay is about two cents extra per litre on top of the usual diesel price, which is not enough to cover the cost of manufacturing biodiesel from a sustainable feedstock.

With inedible tallow now attracting higher prices from overseas biodiesel manufacturers that sell into subsidised markets, the choice of whether to re-open or wind down the plant depends on a more certain set of decarbonisation policies.

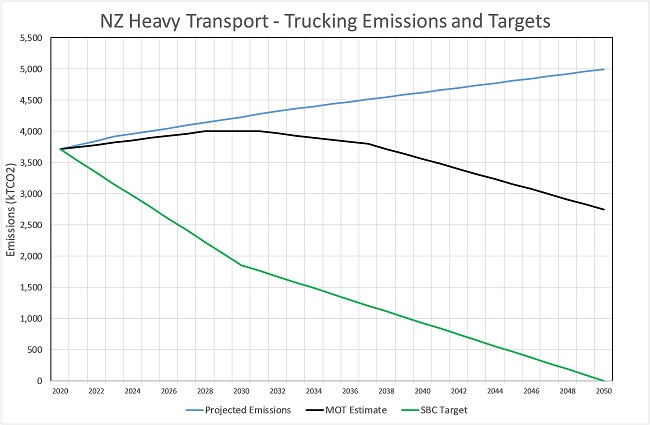

And I must admit seeing the required emissions trajectory on the graph was a stark reminder of the huge effort we need to make in a short space of time. But at the same time I am heartened by what we already know about the solutions and what needs to be true to get them adopted at scale. That’s a key output for this work, which will be completed at the beginning of October.

The power of collaboration also became apparent. This groups’ involvement in each others’ value chain, as well as their knowledge of what it’ll take their own businesses to transition, meant they were quickly able to test assumptions and fill in gaps. When you’re transition planning in your own business there’s often crystal ball gazing questions like “what will our operations look like in ten years time?” and “what will be the maximum price we’re willing to pay for that lower emission piece of kit”. This group are grappling with similar questions, but on behalf of the entire freight system, especially when there are so many interdependencies and trade offs that need to be factored in.

Those readers who are grappling with influencing scope 3 emission reduction will appreciate how easy it is to state what needs to change, but how complex some of the system shifts really are. How would customers react if they were offered a low carbon 3 day delivery offer at a cheaper price than an overnight delivery high carbon offer? It’s worth noting a lot of goods purchase online are often freighted free of charge if a certain amount is spent – so this actually represents a real shift in market expectation and willingness to engage.

So where to next on the journey to a decarbonised freight sector? The consultants will continue to develop the pathway content, taking the feedback from the workshop and tweaking some of the solutions.

Then they’ll shape the recommendations – what are the priority activities and the supporting frameworks to enable them to scale. Our group will meet again at the beginning of August to review the updated pathway, and strengthen their recommendations. We’ll likely have a further workshop before publishing the pathway in October.

Contact: Kate Ferguson, SBC Climate Programme Manager

Phone:

Email: